On 1 July 2026, the EU quietly closed one chapter of its trade policy and opened another. The steel safeguard measure that had governed imports since 2018 expired on 30 June 2026, and in its place a new, permanent instrument — the EU Steel Regulation — entered into application [1][2]. For anyone buying, selling or converting tinplate (ETP) and tin-free steel (TFS/ECCS), the change is not cosmetic: the duty-free space is roughly half of what it was, the penalty for exceeding it has doubled to 50%, and the door is allocated country by country in a way that reshuffles sourcing strategies.

Here is what changed, why it matters, and how we got here.

Two legal acts define the regime:

Regulation (EU) 2026/1384 (“the Steel Regulation”), adopted by the European Parliament and the Council on 17 June 2026, entered into force on 25 June 2026 and opened tariff quotas of 18,345,922 tonnes across 26 product categories, with the out-of-quota duty set at 50% ad valorem [3]. Unlike the safeguard — a temporary trade-defence measure with a legal expiry date — this is ordinary EU legislation designed to address global overcapacity on a durable basis, with built-in review clauses rather than a sunset. It also introduces a “melt-and-pour” traceability requirement, and its a definition still moving. The Commission ran a stakeholder consultation (4 June – 2 July 2026) on what documentary evidence will be accepted to prove the country of melt and pour (e.g., mill test certificates), and the Implementing Act setting the actual requirements is expected only by 31 August 2026, entering into force on 1 October 2026. So, as of today, the precise evidence buyers/importers will need to provide isn’t fixed yet , In conclusion: Documentation requirements are expected to be finalized by the end of August, with duty from 1 October 2026, but only starts influencing quota allocation from 1 October 2027.[3]

Commission Implementing Regulation (EU) 2026/1457 of 29 June 2026 distributes those quotas among trading partners. It applies from 1 July 2026 to 31 December 2026, covering the first two quarters of the new regime, after which a successor implementing act will set the next allocation [3]. The distribution follows the MFN/FTA split described above, and explicitly grants Ukraine a more preferential distribution than other FTA partners in light of its situation as a candidate country [3].

The Commission confirmed the regime’s entry into application on 1 July 2026, presenting it as a step to secure the long-term viability of a strategically crucial European industry against global overcapacity [2].

What it means for tinplate and TFS: Category 6 in detail

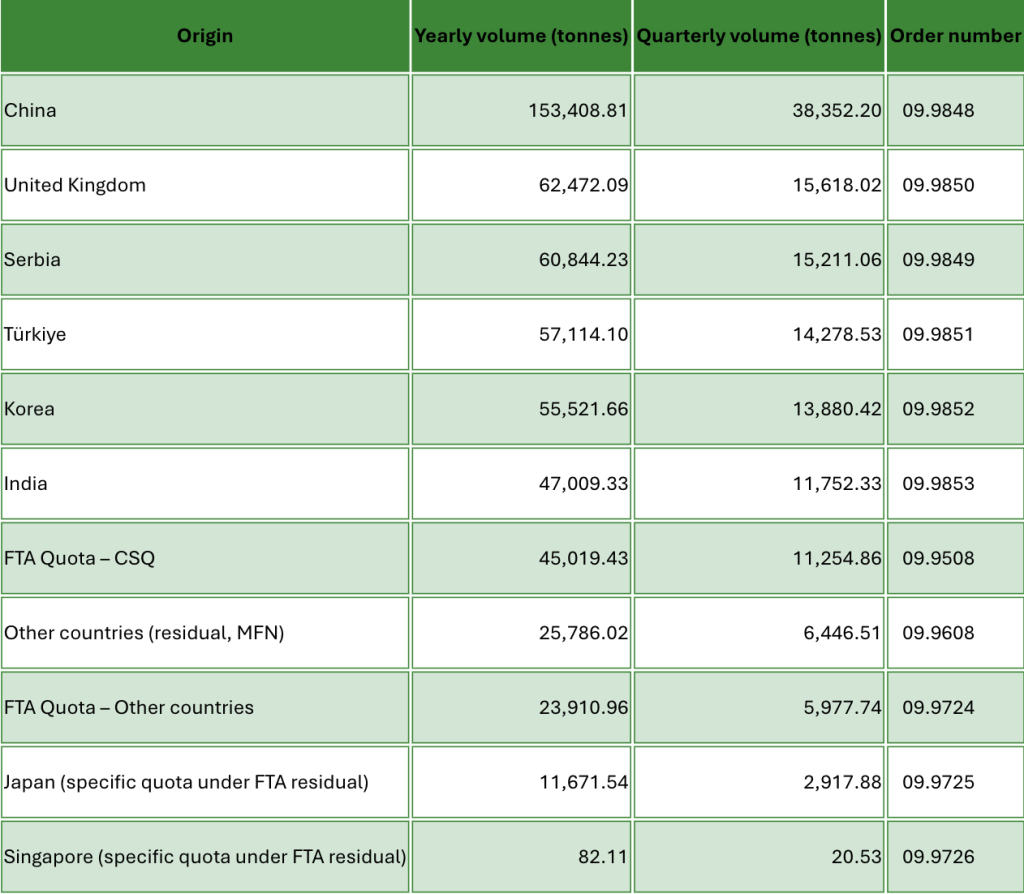

Tin mill products — electrolytic tinplate, tin-free steel/ECCS and blackplate — sit in product category 6, defined by CN codes 7209 18 99, 7210 11 00, 7210 12 20 (TP), 7210 12 80, 7210 50 00 (TFS/ECCS), 7210 70 10, 7210 90 40, 7212 10 10, 7212 10 90 and 7212 40 20 [3].

The annual duty-free volumes allocated in Annex I of Regulation 2026/1457 for category 6 are [3]:

Summing the Annex I lines, the total duty-free space for tin mill products comes to roughly 543,000 tonnes per year (author’s calculation from [3]) — a fraction of the quarterly volumes the market grew accustomed to under the safeguard, as the chart below makes visible.

A few operational notes for buyers:

- China’s quota is MFN-only (FTA part = 0), and China is excluded from the residual “Other countries” quota in category 6 — once its 153,409 tonnes are gone, Chinese material pays 50% [3].

- FTA partners with a country-specific quota (Serbia, UK, Türkiye, Korea, India) get a second life: once their own quota is exhausted, they can compete for the additional 45,019-tonne “FTA Quota – CSQ” on a first-come, first-served basis [3].

- Japan and Singapore hold carved-out volumes inside the FTA residual quota rather than country-specific quotas [3].

The evolution: how we got to the cliff

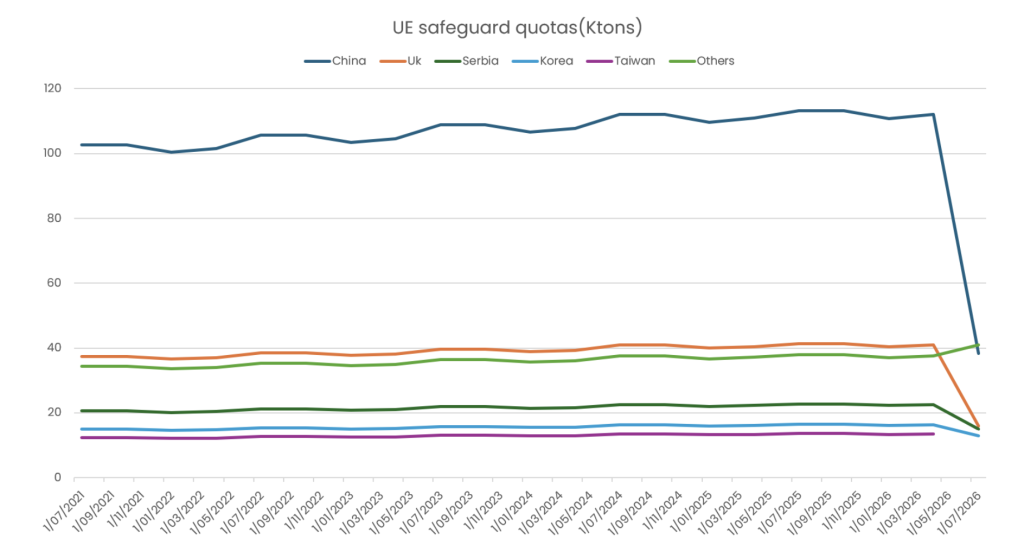

The chart below tracks quarterly duty-free quota volumes for category 6 by origin from July 2021 through the estimated first quarter of the new regime (Q3 2026). The story it tells is one of remarkable stability — quotas were liberalised by small annual increments under the safeguard — followed by an abrupt step-down as the new permanent regime takes over.

EU safeguard quotas evolution, Category 6 — Tin Mill Products, 2021–2026

Figure: Quarterly EU duty-free quota volumes (kt), Category 6 — Tin Mill Products, by origin, July 2021 – July 2026 (last data point estimated under the new regime). Source: Steelforce Packaging analysis based on Implementing Regulations (EU) 2019/159, 2021/1029, 2022/434, 2024/1782 and 2025/612, and DG TAXUD quarterly quota data.

The headline framing — a total quota 47% smaller than the 2024 level, with a 50% out-of-quota duty replacing the previous 25% — was set when Parliament and Council reached political agreement in April 2026 [5]. For tin mill products specifically, the visual is stark: China’s quarterly duty-free access drops from around 110 kt under the safeguard to roughly 38 kt, with every other origin stepping down proportionally.

What to watch next

Three dates matter for planning. 1 October 2026: melt-and-pour evidence becomes mandatory at customs [4]. 31 December 2026: the current implementing regulation lapses and a new allocation act takes over, alongside the first product-scope review [3][4]. 1 October 2027: melt-and-pour data starts influencing country distribution — a potential problem for origins that re-roll imported substrate [4].

For tinplate and TFS buyers, the practical takeaway is that quota monitoring is no longer a compliance afterthought — it is a pricing input. With quarterly windows this narrow, whether a coil lands in week 1 or week 13 of a quarter can be the difference between duty-free and +50%.

References and supporting extracts

[1] European Commission, DG Trade — “Factsheet: EU steel measure.” https://policy.trade.ec.europa.eu/enforcement-and-protection/protecting-eu-steelmaking/factsheet-eu-steel-measure_en

[2] European Commission press release IP/26/1484 (30 June 2026) — “New rules to protect EU steel industry from damaging impacts of global overcapacity enter into application.” https://ec.europa.eu/commission/presscorner/detail/en/ip_26_1484

[3] Commission Implementing Regulation (EU) 2026/1457 of 29 June 2026, OJ L, 30.6.2026. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202601457

[4] Reed Smith, Trade Compliance Resource Hub (26 June 2026) — “EU Steel Regulation published: Key features, application dates, and what to do next.” https://www.tradecomplianceresourcehub.com/2026/06/26/eu-steel-regulation-published-key-features-application-dates-and-what-to-do-next/

[5] Insight EU Monitoring (14 April 2026) — “EU Commission welcomes political agreement on new EU steel measure.” https://ieu-monitoring.com/editorial/eu-commission-welcomes-political-agreement-on-new-eu-steel-measure/1005807